Welcome to the latest Directors Market Report for the period January 2023 Q1. The current market seems very doom and gloom at the moment, however the feedback from contractors is in the contrast! Contractors are taking the new year on strong with confidence and a positive outlook on what is to come this year!

The Construction Purchasing Managers’ Index (PMI) for December 2022 fell into negative territory for the first time since last August and to its lowest reading since May 2020.

A similar trend was reported for new orders, with its steepest fall for more than two-and-a-half years.

Concurrently, sentiment among construction firms towards the year ahead outlook for activity dipped into negative territory for only the sixth time on record, reflecting fears around the near-term economic outlook, the survey authors said. Pessimistic expectations were reflected in the first round of job shedding in the construction sector since January 2021.

The headline seasonally adjusted S&P Global / CIPS UK construction PMI was 48.8 in December, down from 50.4 in November – anything below 50.0 indicates a contraction in construction sector output.

Although commercial construction activity continued to rise in December, at 50.3 its growth was marginal and outweighed by contractions across the residential and civil engineering sectors. House-building activity (48.0) declined for the first time since July 2022; civil engineering recorded a sixth consecutive monthly contraction in output (46.8).

December data also highlighted a reduction in new orders placed with UK constructors, following a modest uplift in November. According to survey respondents, the fall was driven by weak client demand, linked in turn to higher prices charged.

Confidence amongst constructors dropped into negative territory for the first time since the initial covid-19 wave and for only the sixth time on record. Downbeat sentiment was attributed to expectations of a recession and poor demand conditions, as well as inflationary pressures.

Average lead times for inputs lengthened, with delays the most severe since last June. Shortages and shipping issues were cited as the cause. Costs faced by construction companies continued to increase, with energy, materials, fuel and import costs all cited by panellists. However, the rate of inflation was the weakest for two years.

Lewis Cooper, economist at S&P Global Market Intelligence, which compiles the survey said: "The UK's construction sector registered a relatively poor finish to 2022, with business activity falling into decline following a three-month growth sequence amid the fastest contraction in new work since the initial pandemic period in May 2020. Companies cited weak client demand, driven partly by higher prices amid ongoing inflationary pressures.

"Commercial construction activity remained the only bright spot, though here the rate of growth came close to stalling, with the overall contraction led by a further sharp decline in civil engineering and the first fall in residential construction activity since last July."

"The challenging environment in December was subsequently reflected in pessimism amongst firms towards activity levels over the coming year, with business confidence downbeat for only the sixth time since the survey began in April 1997.

"With the outlook turning negative, staffing levels declined for the first time since the start of 2021 in December. Though panellists primarily attributed the fall to the non-replacement of leavers, the data show that companies are preparing to face significant challenges in the months ahead."

John Glen, chief economist at the Chartered Institute of Procurement & Supply, said: "The construction sector was stuck in the mud in December with the steepest fall in activity since the beginning of the pandemic in May 2020 and a similarly fast drop in pipelines of new work.

"House building saw a notable change of direction, with a mix of higher inflation for raw materials and transportation and the squeeze on affordability rates for mortgages resulting in fewer house sales. The sector subsequently fell back into contraction for the first time since July. Civil engineering, responsible for larger projects, continued to be the weakest performer again, with a sixth month in the doldrums as uncertainty about the UK economy reared its ugly head again and customers hesitated. Supply chain managers reined back spending on materials with the sharpest fall in buying activity for over two-and-a-half years as a result of this poor demand.

"Optimism remained very flat and at one of the starkest rates in the survey’s history. Builders were reining back on recruitment unconvinced there will be enough growth in the UK economy in 2023 to justify additional expenditure when margins remained so squeezed. Builders are fast running out of the resilient spirit maintained over the last couple of years as the blocks to success piled up and the winter of discontent with high inflation, strikes and shortages continues."

Mark Robinson, chief executive of local authority procurement agency Scape, said: “After a drop off in activity towards the back end of last year, December’s figures are further evidence of the recession strengthening its grip on the economy.

“The construction industry is braced for a tough year and, while there are positive signs that inflation has peaked, increased material costs will undoubtedly continue to shape the plans of developers and local authorities – that latter of which will be confirming their annual budgets this month.

“Maintaining clear, positive dialogue in 2023 will be crucial if projects are to progress uninhibited, and calm and cautious management will likely pay dividends further down the line when purchasing decisions are ready to accelerate again.”

Fraser Johns, finance director with regional building contractor Beard, said:

“While many within the industry would have been encouraged by the past few months of marginal growth in activity, news of a poor December and end to the year will come as no surprise given the deluge of challenges the sector is facing.

“The higher cost to borrow, tighter access to credit and wider inflationary pressures have had a major impact on client confidence. Contractors, who have seen higher material costs erode margins are now seeing the market for new work tighten, making tenders more competitive. While those with strong balance sheets may be able to stomach that, those already at risk face a difficult 12 months ahead.

“A rise in commercial construction activity – albeit only marginally, is certainly a positive to take from a challenging month. However, it may not be enough to rescue the general optimism of the sector, especially as civil engineering and residential construction stumbled. While resilience may be tested, the mantra has to be to “control what we can control” moving forward, working closely with developers, clients and stakeholders.”

Construction output in Great Britain: November 2022

1.Main points

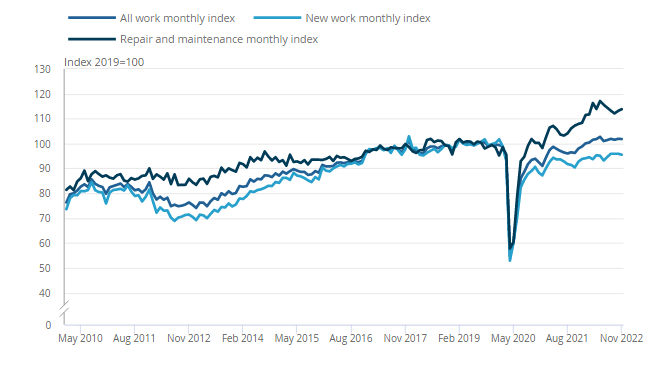

- Monthly construction output is estimated to have flat growth (0.0%) in volume terms in November 2022; this follows a downwardly revised increase of 0.4% in October 2022.

- The flat growth in monthly construction output in November 2022 came from a decrease in new work (0.4% fall), offset by an increase in repair and maintenance (0.6%) on the month.

- At the sector level, the main positive contributors to the flat growth were seen in infrastructure new work and non-housing repair and maintenance, which increased 4.2% and 2.4%, respectively; the main negative contributors were seen in private new housing and private housing repair and maintenance, falling 4.8% and 1.7%, respectively.

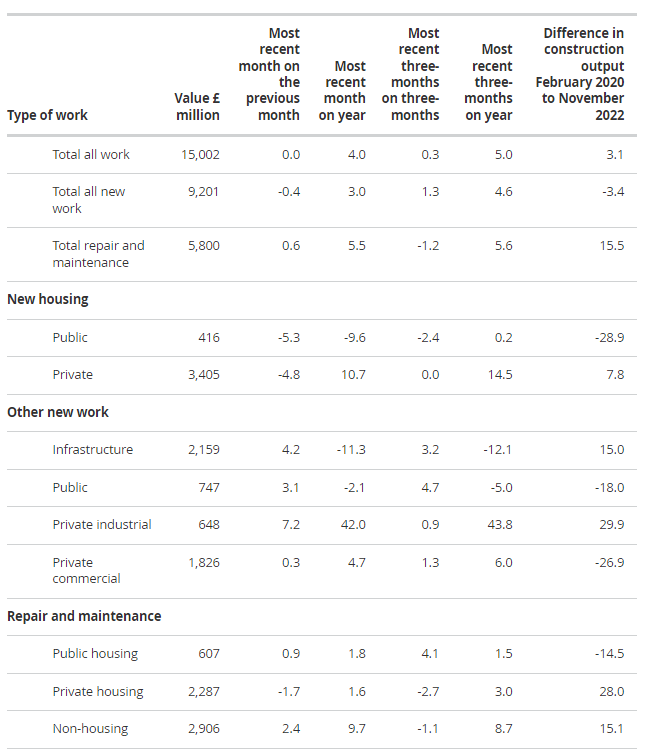

- The level of construction output volume in November 2022 was 3.1% (£452 million) above the February 2020 pre-coronavirus (COVID-19) pandemic level; new work was 3.4% (£327 million) below its February 2020 level, while repair and maintenance work was 15.5% (£778 million) above the February 2020 level.

- Construction output saw an increase of 0.3% in the three months to November 2022; the increase came solely from growth in new work (1.3%) as repair and maintenance saw a decrease (1.2% fall).

- Revisions in this release are seen back to January 2021 and are consistent with the Gross domestic product (GDP) quarterly national accounts, UK: July to September 2022 bulletin, published on 22 December 2022.

2.Construction output in November 2022

Monthly construction output growth was flat (0.0%) in November 2022. This follows a downwardly revised 0.4% increase in October 2022.

Figure 1: The monthly all work construction output index in November 2022 saw flat growth on the month coming from a decrease in new work (0.4%) offset by an increase in repair and maintenance (0.6%)

Monthly all work index, chained volume measure, seasonally adjusted, Great Britain, January 2010 to November 2022

Anecdotal evidence received from returns for the Monthly Business Survey for Construction and allied trades (MBS) suggested that the narrative around increased prices for certain construction products is less notable this month, with fewer businesses reporting struggles in relation to costly materials. However, more businesses are starting to further reference economic worries leading to customers delaying or cancelling work than in previous months.

To a lesser extent, additional comments mentioned heavy rainfall throughout November 2022. The Met Office confirmed in their Monthly climate summary (PDF, 363KB) that rainfall was above average and businesses cited that for the construction industry, the rain caused difficult working conditions. However, for some businesses the rainfall generated more work relating to repairs.

Detailed growth rates

Table 1: Construction output main figures, November 2022, Great Britain

Seasonally adjusted, chained volume measure, £ million and percentage change

Month-on-month construction output growth in November 2022

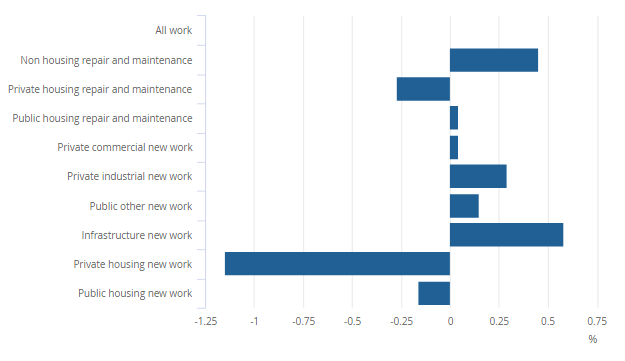

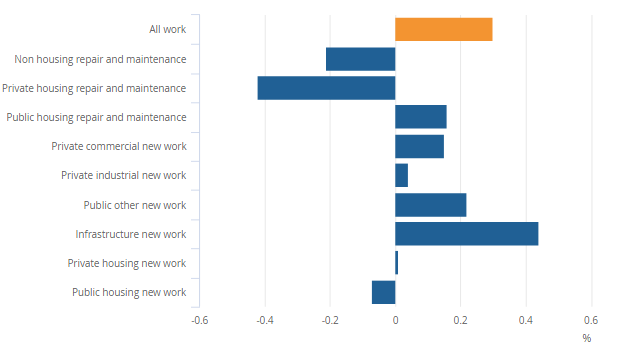

The 0.0% monthly growth in construction output in November 2022 was a mixed picture, with six out of the nine sectors seeing an increase on the month.

Figure 2: All work saw flat growth on the month in November 2022 (0.0%) with six of the nine sectors seeing an increase

Contributions to monthly growth (November 2022 compared with October 2022), chained volume measure, seasonally adjusted, Great Britain

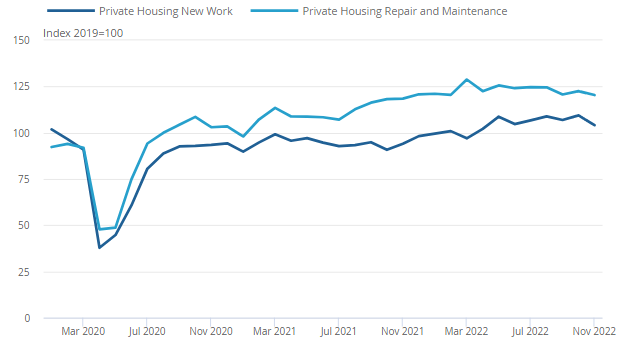

Private new housing and private housing repair and maintenance were the largest negative contributors to the flat growth in November 2022, decreasing 4.8%, (£172 million) and 1.7% (£41 million), respectively. The largest positive contributions were from infrastructure new work and non-housing repair and maintenance, increasing 4.2% (£87 million) and 2.4% (£68 million), respectively.

The large decrease in private new housing follows an increase of 2.3% in October 2022 (£81 million), whereby private new housing was the largest contributor to the increase to monthly growth in October 2022. Private housing repair and maintenance also showed a similar profile, following an increase of 1.4% in October 2022. Anecdotal evidence suggests a general reduction in housing work in November 2022, however, both are still above their pre-coronavirus levels (Table 1).

Figure 3: Both private housing sectors show monthly decreases in growth in November 2022 following increases in October 2022

Private new housing and private housing repair and maintenance, index volume measure, seasonally adjusted, Great Britain, January 2020 to November 2022

Three-month on three-month construction output growth in November 2022

Construction output rose slightly by 0.3% (£140 million) in the three months to November 2022. This is the first increase in the three-month on three-month series since July 2022 (0.5%). However, it is important to note that the weak June 2022 (negative 1.7%), where two working days were lost because of the Queen's Platinum Jubilee, is in the base period. The increase in the three months to November 2022 came solely from a increase in new work (1.3%) as repair and maintenance decreased (negative 1.2%)

Figure 4: All work saw a slight increase in the three-months to November 2022 (0.3%) with infrastructure new work as the main contributor

Contributions to quarterly growth (September to November 2022 compared with June to August 2022), chained volume measure, seasonally adjusted, Great Britain

Of the nine sectors, six saw an increase in the three months to November 2022, with the largest contributors being infrastructure new work, public other new work and public housing repair and maintenance. These sectors increased 3.2% (£199 million), 4.7% (£98 million) and 4.1% (£71 million), respectively.

3.Revisions to construction output in this release

Estimates in this release are consistent with the Gross domestic product (GDP) quarterly national accounts, UK: July to September 2022 bulletin, published on 22 December 2022.

Revisions in this release have been incorporated back to January 2021. Alongside the revisions in the latest quarterly national accounts release, October 2022 is also open for revision in today's publication. For further information as to the reasons for these revisions, see Section 6: Measuring the data.

The revision to the annual rate of construction output growth in 2021 was minimal, revising down 0.1 percentage points to annual growth of 12.8%.

The revisions to the monthly and quarterly rate of construction output growth are larger than normal, however, are of a balanced profile. This is mainly coming from late and revised Monthly Business Survey (MBS) survey data and, to a lesser extent, changes to the seasonal adjustment specification files.

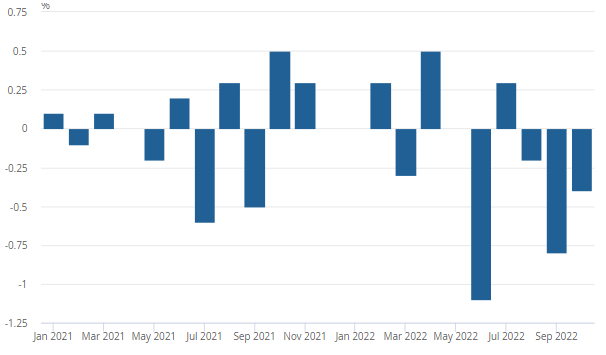

Figure 5 shows the monthly revisions to growth of construction output in this month's release (13 January 2023) compared with last month's release (12 December 2022). Notably, June 2022 and September 2022 saw revisions of a larger magnitude than usual, with falls of 1.1% and 0.8%, respectively. These downward revisions in the latest periods also led to Quarter 3 (July to Sept) 2022 being revised down 0.8 percentage points to a quarterly fall of negative 0.2%.

Figure 5: Late and revised survey data returns contribute to the downward revisions to all work construction output monthly growth in the latest months

Revisions to monthly growth, all work construction output, chained volume measure, seasonally adjusted, Great Britain, January 2021 to October 2022

Source of the Construction output in Great Britain: November 2022 - ons.gov.uk

The latest Builders Merchant Building Index (BMBI) report reveals that builders’ merchants’ value sales were up +7.5% in October 2022 compared to the same month in 2021. Volume sales dropped again (-5.6%) while prices climbed +13.9%, so price inflation was the driving factor of growth.

Save or share

Eleven of the twelve categories sold more in October compared to the previous year, with eight performing better than the Merchants overall. Renewables & Water Saving (+66.1%) was the standout category, while Plumbing, Heating & Electrical (+19.5%), Workwear & Safetywear (+19.0%) and Kitchens & Bathrooms (+17.5%) also had a good month. Timber & Joinery Products (-8.4%) was the only category to sell less.

Compared to pre-pandemic October 2019, total merchant value sales were +19.6% higher in 2022. Volume sales fell -8.9% while prices were +31.2% higher. With two less trading days this year, like-for-like sales were up +31.0%. Four of the twelve categories grew more than total Merchants with Renewables & Water Saving (+59.5%) leading the pack. Landscaping (+31.2%), Timber & Joinery Products (+23.4%) and Heavy Building Materials (+21.5%) also fared well.

Month-on-month, total merchant sales dropped slightly (-0.9%) in October compared to September. Volume sales were also marginally down (-1.8%) and prices edged up (+0.9%). Plumbing, Heating & Electrical (+9.3%) grew most, followed by Tools (+5.4%). Seasonal category Landscaping (-8.1%) was the weakest.

Mike Rigby, CEO of MRA Research which produces this report, said: “The building industry does not operate in a vacuum and this year it’s been hit by the effects of political turmoil and economic UK own goals, and aggressive policies and events in Russia and China. Steeply rising interest rates, soaring energy costs, a cost-of-living crisis, a rapid slowdown in the housing market, plus beneficial freight rates tumbling back to normal, have all impacted the sector.

“Coming after a series of national lockdowns and a prolonged period of furlough, it’s hard to think of a time when the industry has had to face so many shocks to the system in such a short time. And the industry has coped remarkably well. But the roller coaster is not over. The new combination of Sunak and Hunt are safe hands but can they bring their party with them, and will their feet on the brakes postpone productivity improvements and growth? Who knows? And good luck to the boards who must put their budgets to bed before the start of 2023! It would be good to return to some sense of normality in 2023 but I wouldn’t bet on it.”

That's A Wrap!

A lot of points have been covered and I hope this information in the report has been of some use to you. We do try to collate information from as many different areas as possible so please do refer to last quarters report as well for a crossover of information.

We will see you again soon!

If you are already a client of Saint, please feel free to discuss with your business development manager to discuss this report and to provide specific data for your sector.

The Construction Survival Guide

The only book you need to start up your construction business! The CSG becomes your new handbook offering everything that you need in order to create a successful construction business!

Claim Mine!

This article has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the provided content.

PS. Whenever you are ready, here's how to grow your construction business...

1. Join our Facebook Group which built completely for businesses within the construction industry. Real people, real support. - Now also available on LinkedIn.

2. Keep up to date with Construction Insider Providing you with industry insight, tips & tricks and much more to make sure you are ahead of your competitors!

3. When you are ready, Become a Saint Global client, and we will provide you with the highest quality solutions to effectively scale your construction business. Book your meeting here!

Written by the team at: