Hi and welcome to this months market report up to June end 2022

As usual we start with the data back from the likes of Screwfix, Victorian Plumbing and Topps tiles as an indicator of not only the smaller contractor purchases but also as a guide to the confidence in this sector and then we will move onto the heavier trade indicators.

B & Q / Screwfix

Owners Kingfisher says online sales now represent 16% of group sales, following 164% ecommerce growth over the last three years.

B&Q sales, said Kingfisher, were hit by February’s UK storms but saw “resilient” demand for kitchens, bathrooms and storage, while trade sales through TradePoint accounted for 21% of sales in the first quarter.

The update comes as Kingfisher reports first quarter figures showing a fall in year-on-year sales as the retailer moves beyond the peaks of lockdown trading. Group sales came in at £3.2bn in the three months to April 30. That’s 5.8% down on the same time last year, in total. Sales are 5.4% down on a like-for-like, constant currency basis that strips out the effect of any store openings and closures and of foreign exchange fluctuations. But they are also up by 16.2% LFL, constant currency, up on three years earlier – the last pre-pandemic comparative period.

In the UK and Ireland, sales of £1.6bn were 14.2% down on last time, and 15.8% down on the same LFL, constant currency basis. Compared to three years earlier sales were 16.7% ahead. Sales of £996m at B&Q were a total of 17.8% down on last time, and 16.3% LFL up on three years earlier. Screwfix sales of £572m were down on last year (-7.1%) but up on three years ago (+18%).

In the first two weeks of the second quarter, to May 14, group LFL sales were 2.5% down on last year, and 21.8% ahead of three years ago.

“We continue to effectively manage inflationary and supply chain pressures. As a result, our product availability is now very close to ‘normal’ levels across all our banners, and we continue to deliver value for our customers through our own exclusive brands and competitive prices.”

Victorian Plumbing

Victorian Plumbing reported revenue of £133.9m in the six months to March 31. That’s 5% down on the same time last year and 39% ahead of the same period two years ago. Pre-tax profits of £2.7m were 81% down from £14.5m a year ago, and 65% down on two years ago as costs rose. Adjusted EBITDA (earnings before interest, tax and asset writedowns) of £6.7m was 67% down on last year, and 24% down on two years ago. Looking ahead, it expects modest growth in the rest of the year and will also continue to take a careful approach to price rises.

First-half trade revenue was 18% up on the previous year, at £24.6m and accounted for 18% of total sales.

Matthew Walton, senior retail analyst at Global Data, says: “Victorian Plumbing still expects to record modest growth for the full year, despite these challenging interim results. To help achieve this, it needs to build on the traction it is starting to achieve within trade, which accounted for 18.4% of sales during the period, a 3.5 ppts uplift on last year.

Topps Tiles

Topps Tiles has expanded its trade business – acquiring Pro Tiler in March during a half year in which commercial revenue grew by 24% to £5m.

However, it points to a range of challenges during the first half, from supply chain disruption to the effects of war in Ukraine.

Today’s update comes as Topps Tiles today record first-half turnover of £119.2m in the six months to April 2 2022. That’s 15.5% up on the previous year. Pre-tax profits of £5.6m are 40% up from £4m a year earlier.

In the first seven weeks of the second half, like-for-like sales grew by 5.7%. In the most recent five weeks, like-for-like sales were slightly below the same time last year – which followed the end of the third UK lockdown, in which non-essential shops had to close.

Supply Chain Disruption

Topps Tiles says the first half has been marked by issues including a national shortage of HGV drivers, logistical issues in UK ports and a “dramatic increase” in global shipping costs. At the same time, rising gas prices affected the cost of making tiles around the world and the retailer has had to increase the selling prices of many ranges. It says that economic pressures on some tile producers have been so severe that "in some cases factories have reduced or paused manufacturing".

Topps says availability of labour has been a significant challenge in the first half of the year. "Although the level of staff absence due to Covid-19 has been falling across the first half, our vacancies were higher than we would have liked, reflecting the declining size of the UK workforce set against an economy which was still expanding

The war in Ukraine has added to challenges, both because the country is a significant supplier of clay and because of the continued rise in gas prices.

Market Review

Confidence is low as markets respond to latest data.

Input buying activity rose for the sixteenth consecutive month in May, while stocks of purchased goods rose at the quickest pace in three months.

S&P Global / CIPS UK Manufacturing PMI®

- Output growth at seven-month low

- Consumer goods sector hit by weaker consumer demand

- Input cost and output price inflation remain elevated

Growth in the UK manufacturing sector eased during May, as rates of expansion in output, new orders and employment all decelerated. The slowdown was driven by weaker growth of domestic demand, lower intakes of new export work and ongoing disruption caused by stretched supply chains, rising cost pressures and the war in Ukraine.

The seasonally adjusted S&P Global / CIPS UK Manufacturing Purchasing Managers’ Index® (PMI®) posted 54.6 in May, unchanged from the earlier flash estimate and down from 55.8 in April. The PMI – which is calculated from five subindices – has remained above the neutral 50.0 mark for 24 months.

Manufacturing output increased at the slowest pace since October 2021. The performance of the consumer goods industry was especially weak, with production falling for the first time in 15 months. Growth slowed at intermediate goods producers, but accelerated in the investment goods category.

May saw the weakest increase in new work received during the current 16-month sequence of expansion. Supply chain issues, subdued client confidence, signs of economic slowdown and reduced export order intakes all stymied new order growth.

New orders declined in both the consumer and intermediate goods sectors. The downturn in the former also reflected the impact on consumer demand of the current cost of living crisis. Investment goods producers saw new work intakes rise at a quicker pace.

May saw new export orders decline for the eighth time in the past nine months. Companies attributed lower inflows of new work from overseas to Brexit difficulties, transportation delays, shipping disruptions and the loss of orders due to the war in Ukraine.

Weaker growth of new orders led to reduced backlogs of work and increased holdings of finished goods inventory. Stock levels rose due to intentional replenishment and delays in the despatch of finished goods to clients.

Stretched global supply chains and the associated scarcity of certain inputs also contributed to input price increases and rising levels of purchasing to build-up safety stocks.

Input cost inflation stayed substantial in May, easing from April's near-survey record high. Chemicals, energy, food, freight, fuels, gas, metals, oil, plastics, polymers, timber, and transportation (air, land and sea) were all reported as being up in price. China lockdowns, exchange rate factors, sanctions on Russia, the war in Ukraine, supply chain disruption and raw material scarcity also drove up purchasing costs.

Part of the increase in input costs was passed on to clients in May. Selling prices rose at a rate close to April's survey record high. The increase was linked to inflationary pressures, material shortages and rising labour and energy costs.

Input buying activity rose for the sixteenth consecutive month in May, while stocks of purchased goods rose at the quickest pace in three months. Rising demand for materials combined with stretched global supply chains led to longer delivery times from vendors. That said, lead times increased to the weakest extent in over a year-and-a-half, suggesting that the pressure on supply chains was past its peak.

UK manufacturing employment rose for the seventeenth successive month in May, albeit at the slowest pace since last October. The outlook for the sector remained positive, with 55% of manufacturers expecting output to rise over the coming year. However, confidence slipped to a 17-month low, amid fears of a possible global recession, rising cost pressures and stretched world supply chains.

Rob Dobson, Director at S&P Global Market Intelligence, said: “The rate of expansion in UK manufacturing output eased to a seven-month low in May as companies face a barrage of headwinds. Factories are reporting a slowdown in domestic demand, falling exports, shortages of inputs and staff, rising cost pressures and heightened concern about the outlook given geopolitical uncertainties. The consumer goods sector was especially hard hit, as household demand slumped in response to the ongoing cost of living crisis.

With both input costs and selling prices rising at rates close to April's peaks, the surveys suggest that there is no sign of the inflationary surge abating any time soon. Manufacturers continue to report issues getting the right materials, at the right time for the right price, and energy prices remain a major concern.

“Forward-looking indicators from the survey suggest that a further slowdown may be in the offing. Business optimism dipped to a 17-month low and weaker demand growth led to surplus production, meaning warehouse stock levels are rising. Any reversal of this stock-building trend could reinforce the drag of other headwinds and add to downside risks to the outlook.”

Duncan Brock, Group Director at the Chartered Institute of Procurement & Supply: “A softening in overall output growth amongst manufacturing companies in May revealed the slowest rate of expansion since October as supply chain managers pointed to war disruptions and unrelenting price hikes as reasons for this unwelcome trend. “

Though new order levels rose for the sixteenth month they were noticeably softer and driven largely by the domestic market. Export levels fell, hindered by Brexit customs controls and general global disruption. This was especially evident in the consumer goods sector which suffered a sharp fall in overall output as nervous consumers concerned about rising food and energy costs reined back their spending.

“Though the strain on vendor performance eased there is little in this month’s figures to encourage the manufacturing sector and optimism fell to a 17-month low. Suffering a potent cocktail of more disruptions, rising cost pressures and a go-slow UK economy, businesses will be on a knife edge that any business decisions will be the right ones for the coming months.

Merchants and Sectors

Builders’ merchant sales bounce back in May

The latest figures from the May Builders Merchant Building Index (BMBI) report reveal a sharp rise in sales as lockdown restrictions ease and trades return to work.

Year-on-year, Total Builders Merchants value sales in May were down -39.9% compared with May 2019, reflecting the cautious reopening of merchant branches with many still operating a restricted service. However, the overall trading figures are a significant improvement on April 2020 sales (-76.3%).

A closer look at how individual product categories performed in May reveals that year-on-year,

Tools (-66.1%) and Kitchens & Bathrooms (-62.7%) have been hit hardest by the pandemic lockdown. Timber & Joinery Products were also down by 40.5% over the same period, however month-on-month, the category is showing some green shoots of recovery with sales more than tripling compared to April 2020 (+199.5%). Heavy Building Materials, the largest product category, was down 39.0% year-on-year but showed a substantial month-on-month improvement on April 2020 (+157.6%).

The biggest winner in May was Landscaping, with sales of this seasonal category down just -12.5% on May 2019. This is a remarkable recovery from April, when sales were down a massive -74.4% compared to April 2019. Workwear & Safety wear was less affected by the lockdown, with demand for PPE continuing to drive sales.

The BMBI is a brand of the Builders’ Merchants Federation, developed and produced by MRA Marketing. The Index uses GfK’s Builders Merchant Point of Sale Tracking Data which analyses sales out data from over 80% of generalist builders’ merchants’ sales across Great Britain, making it the most reliable source of data for the sector.

BMF CEO John Newcomb comments: “As expected, May’s sales figures show a huge year-on-year decline, but they also indicate the strength of the initial bounce-back from April’s COVID-19 crash low-point. The massive effort by the entire supply chain to develop and implement COVID-secure working practices to enable the safe and rapid re-opening of manufacturing facilities, merchant branches and construction sites can be seen in May’s results. There is a long way to go on the road to recovery, but we can look on this as a positive first step.”

Emile van der Ryst, Senior Client Insight Manager – Trade at GfK adds: “The Builders Merchants sector has seen a strong and expected recovery from April’s lockdown as the core categories of Heavy Building Materials, Timber & Joinery and Landscaping drive market activity. May growth is still down by -40% from last year, with the next couple of months critical. Favourable weather conditions and relaxed restrictions will hopefully provide the platform for these core categories to recover some of the losses seen during lockdown.”

Anecdotal evidence indicates that starting new projects is being hampered by the volatility in market prices of materials and hence an inability or difficulty to agree fixed price contacts. The larger the project the greater the risk and therefore perhaps unsurprisingly, the new starts recorded in the crane survey data in this period are generally much smaller schemes.

Trades are clear that prices are only going one way - up!

Sentiment around both costs and prices is very clearly moving upwards, and significantly. 12 months ago, trades were predicting an average rise over the following 12 months of around 3.4% for commercial office projects, and 3.0% for fit out projects. In our previous survey, six months ago, these numbers had increased to 8.1% and 5.9%, respectively. In our latest survey trades are predicting an increase of 10.8% for office projects and 7.6% for fit-out projects. The rate of increase for offices is higher as this reflects the exposure to significant increases in energy prices that affect materials such as the steel, cement and glass.

The fixed price nature of many construction projects means that contractors are working on projects that they priced 12 or 18 months ago and are now facing thin or more likely negative margins, the impact of which may play out in the coming months. As described above, the ability to close out contract negotiations on new projects will inevitably lead to delays and/or the need to consider risk sharing between contractors and clients.

The Construction Leadership Council has set out plans to mitigate the impacts of steep inflation that are hitting companies across the sector. The recent Ukraine crisis has compounded existing challenges of materials’ supply and prices, caused by the aftereffects of Covid-19, escalating global demand, and supply chain disruptions. This has resulted in difficulties in both the availability and cost of many key materials used by the sector, with cost increases of 50% reported for some products in recent weeks.

The Construction Leadership Council has brought together experts from across the sector to look at the options available to reduce these impacts. It is recognised that many of the factors driving the materials crisis are outside the control of businesses and the UK Government. However, where it is possible to act, the CLC is seeking to co-ordinate industry effort to minimise risk and reduce the impact of inflation where it can.

The CLC’s plan includes:

- Developing market intelligence about risk hotspots;

- Publishing guidance on price inflation indexation, and commercial issues;

- Preparing case studies on good practice in response to current inflation;

- Running industry briefings on conflict avoidance;

- Researching long-term capacity loss from Ukraine, Russia and Belarus, and impacts on sector. Further information will be published in the coming weeks.

The CLC is also seeking views from the sector about how the current crisis is affecting businesses from across UK construction, to guide and inform further action. CLC member and Mace Group Chairman and Chief Executive Mark Reynolds said: “Across our industry we are seeing businesses facing real challenges with inflation that are well above those seen in the sector for many years.

There is no one party that can tackle this issue alone and we can’t pass the problem on to others to solve. We all must work collaboratively – clients, contractors and everyone in our supply chain – to provide support where possible to limit the impact on firms nationwide”

Construction Product Availability Statement

31 May 2022

Price inflation and a diminishing labour supply are now of greater concern than product availability in most construction sectors. In terms of availability, little has changed since our last report, with a good supply of most products and materials. Ongoing challenges continue to affect bricks, air crete blocks, roof tiles, chipboard flooring, gas boilers and other products requiring semi-conductors within sub-components, all of which will be subject to longer lead times throughout the year.

The market is becoming more adept at managing supply of these critical products, and the long-term nature of some of the underlying issues. Although there are reports of delays in supply of boilers leading to extended completion times in new housing, new semi-conductor capacity is coming on stream in late 2023/2024, and expansion in existing capacity will feed into the market over the same timescale.

Demand remains strong in all areas, and this is set to continue into the autumn, although some product forecasts now anticipate a slight slowdown in housing starts towards the end of the year, stemming from rising prices and concerns about affordability. Home improvement work will depend on levels of consumer confidence as costs of living rise.

Members of the group raised concerns regarding the threatened rail strike. This will affect aggregate and concrete deliveries to major infrastructure products, highlighting the need for government to prioritise transport of construction materials should the strike go ahead.

There is, however, some good news from parts of China. With Shanghai gradually removing covid restrictions, production should normalise in that major industrial region by mid-June. Shipping analysts warn, however, that this may exacerbate the current bottlenecks in deliveries to the West. Across the board, managing price volatility and labour are now the biggest issues. Although labour shortages are affecting manufacturers, the greatest concern is expressed by house builders and SME builders, as it takes at least three years to train a skilled tradesperson.

The cost of energy and fuel are major drivers for price volatility.

Initial results suggest energy hedges are short term and very significant increases are expected to come through quite quickly. This will particularly affect energy-intensive products including steel, glass, plasterboard, cement, ceramics and porcelain.

Although steel prices have come down slightly, since initial disruption following the outbreak of war in Ukraine, energy prices remain a major issue and price volatility will continue. Market prices will also be affected by the Indian Government’s unexpected increase to export duties on iron ore and steel, effective from 22 May.

Government Construction Datasets

Short-term measures of output by the construction industry, contracts awarded for new construction work in Great Britain and a summary of the Construction Output Price Indices (OPIs) in the UK for Quarter 1 (Jan to Mar) 2022.

1.Main points

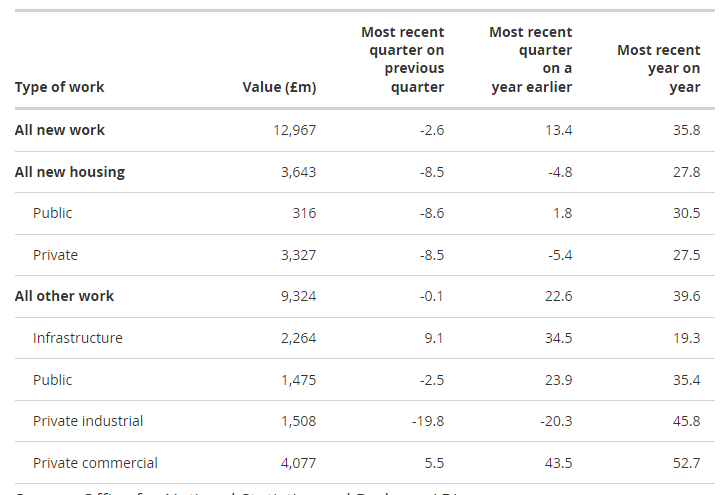

- Monthly construction output increased by 1.7% in volume terms in March 2022; this is the fifth consecutive monthly growth and a record high in monthly level terms (£14,994 million) since monthly records began in January 2010.

- The increase in monthly construction output in March 2022 was driven by increases seen in both repair and maintenance (3.0%) and new work (1.0%); At the sector level, private housing repair and maintenance (5.8%) and private commercial new work (4.0%) were the main contributors to the monthly increase.

- Anecdotal evidence from returns received for our Monthly Business Survey for construction and allied trades suggested storms between 16 and 21 February 2022 resulted in businesses seeing a higher workload in March 2022; this is because of the repair work derived from the storms.

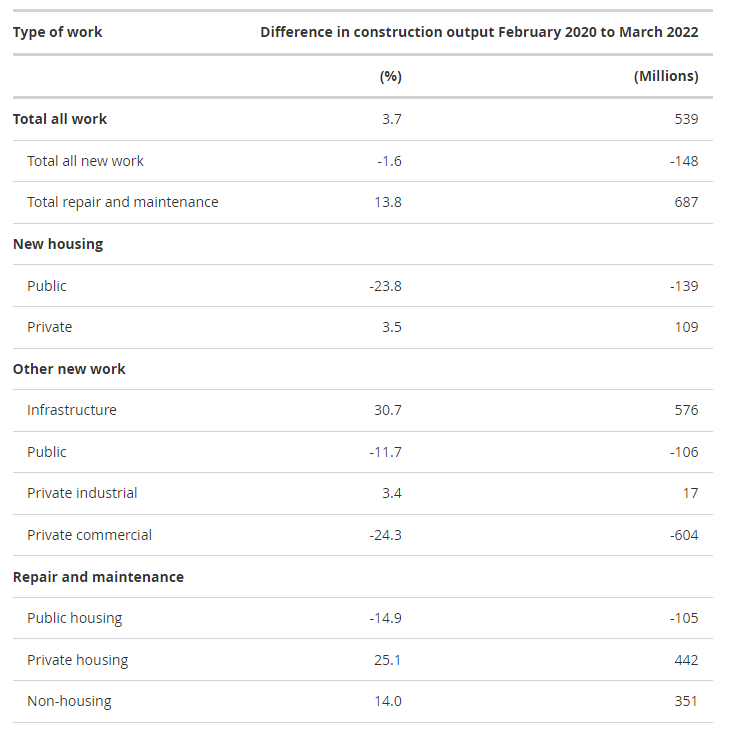

- The level of construction output in March 2022 was 3.7% (£539 million) above the February 2020 pre-coronavirus (COVID-19) pandemic level; new work was 1.6% (£148 million) below the February 2020 level, while repair and maintenance work was 13.8% (£687 million) above the February 2020 level.

- Along with the monthly increase, construction output rose 3.8% in Quarter 1 (Jan to Mar) 2022; outside of the coronavirus pandemic period, this is the strongest quarterly growth since Quarter 1 2017 (3.9%).

- Total construction new orders decreased by 2.6% (£346 million) in Quarter 1 2022 compared with Quarter 4 2021; despite this quarterly fall, all sectors are still above their pre-coronavirus pandemic level (Quarter 4 2019).

- The annual rate of construction output price growth was 7.3% in the 12 months to March 2022; this was the strongest annual rate since records began in 2014.

Estimates for March 2022 are subject to more uncertainty than usual because of challenges we have faced with data collection. This has led to lower response rates than those seen before and during the coronavirus pandemic.

2.Construction output in March 2022

Monthly construction output grew 1.7% in volume terms in March 2022 compared with February 2022. This is the fifth consecutive month of growth and is the largest single-month growth since January 2022 (2.1%). Monthly construction output in March 2022 is now at its highest level (£14,944 million) since monthly records began in January 2010 (Figure 1).

The stormy spells (storms Dudley, Eunice and Franklin) seen between 16 and 21 February brought heavy rain and winds across much of the country. For the construction industry, working days were lost during this time. However, demand continued to be strong; anecdotal evidence received from a number of businesses for March 2022 reported a positive impact because they picked up repair and maintenance work in March caused by the storm damage.

Figure 1: The monthly index shows the level of construction output grew to an all-time high in March 2022, with its fifth consecutive monthly increase

Monthly all work index, chained volume measure, seasonally adjusted, Great Britain, January 2010 to March 2022

Table 1: Construction output main figures, difference in construction output February 2020 (pre-coronavirus pandemic level) to March 2022, Great Britain.

Seasonally adjusted, chained volume measure, percentage change and £millions change

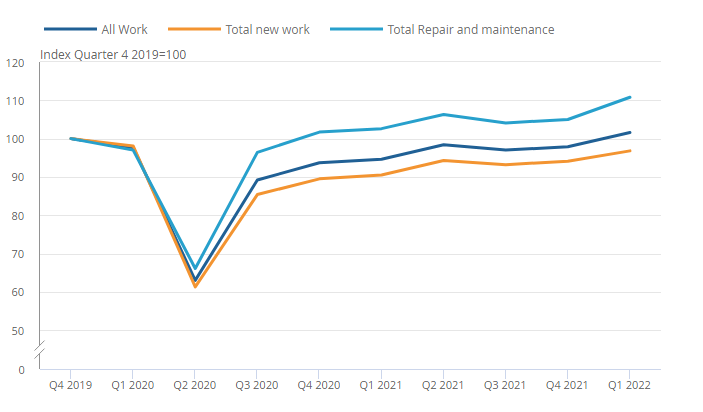

The monthly growth in March 2022, following that seen in January and February, has resulted in the quarterly all work index in Quarter 1 (Jan to Mar) 2022 recovering to above its pre-coronavirus (COVID-19) pandemic level (Quarter 4 (Oct to Dec) 2019) for the first time (Figure 2).

Figure 2: The quarterly all work construction output index recovered above its pre-coronavirus pandemic level (Quarter 4 2019) for the first time in Quarter 1 2022

Quarterly all work index, chained volume measure, seasonally adjusted, Great Britain, Quarter 4 2019 to Quarter 1 2022

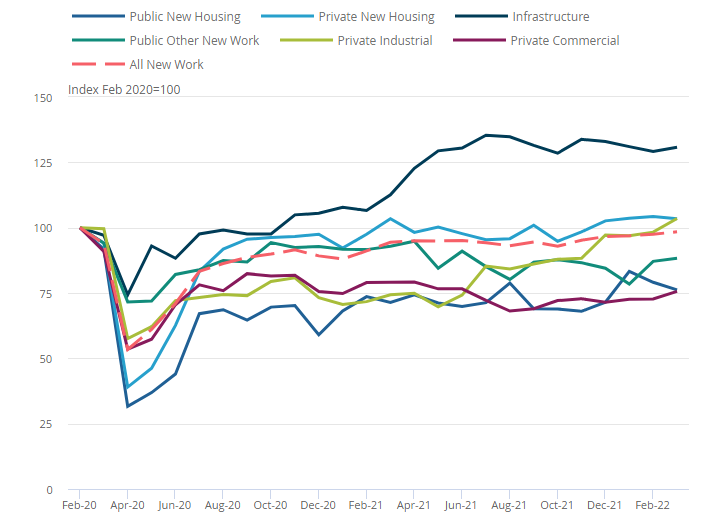

Figure 3: In March 2022 three out of the six new work sectors were above their pre-coronavirus pandemic (February 2020) level of output

Components of new work, index volume measure, seasonally adjusted, Great Britain, February 2020 to March 2022

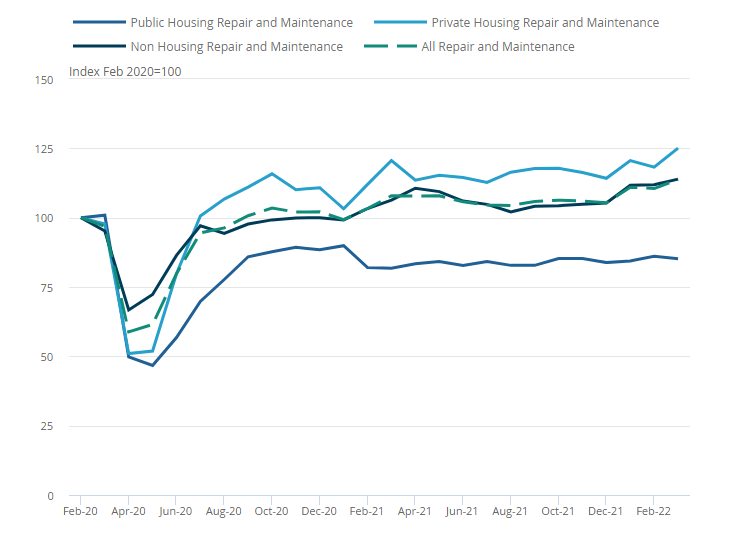

Figure 4: Public housing repair and maintenance was the only repair and maintenance sector to remain below its pre-coronavirus pandemic (February 2020) level

Components of repair and maintenance, index volume measure, seasonally adjusted, Great Britain, February 2020 to March 2022

Detailed growth rates

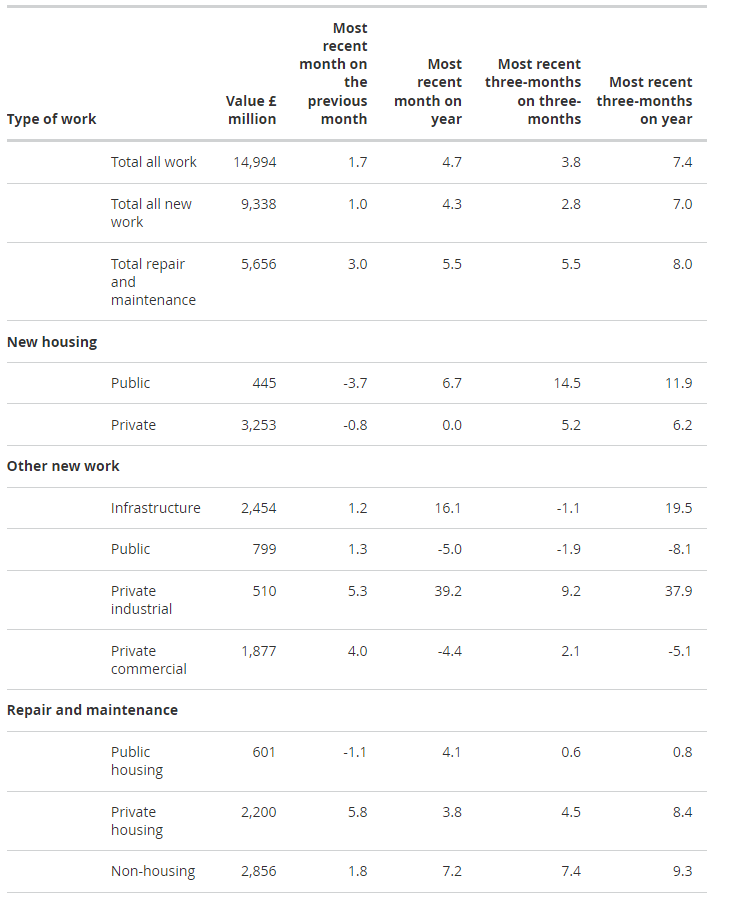

Table 2: Construction output main figures, March 2022, Great Britain

Seasonally adjusted, chained volume measure, £ million and percentage change

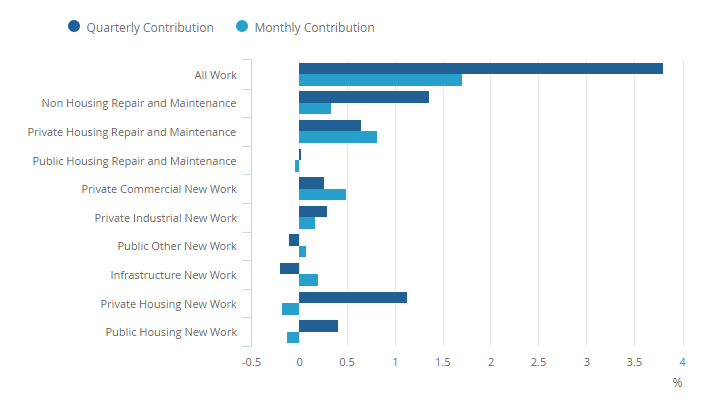

Figure 5: All work saw growth on both the month (1.7% in March 2022) and the quarter (3.8% in Quarter 1 2022)

Contributions to monthly (March 2022) and quarterly growth (Quarter 1 2022), chained volume measure, seasonally adjusted, Great Britain, percentage points

Month-on-month change in construction output in March 2022

Construction output grew 1.7% (£257 million) in March 2022 compared with February 2022.

Private housing repair and maintenance and private commercial new work were the largest contributors to the monthly increases, growing 5.8% (£121 million) and 4.0% (£72 million), respectively. Anecdotal evidence gathered over the month suggests the increases seen in private housing repair and maintenance resulted from businesses seeing a higher workload in March 2022. This higher workload was mostly repair work derived from the storms seen in the second half of February 2022.

Anecdotal evidence from businesses suggests the increase In March 2022 in private commercial came from an increase in offices. This is further shown in the new orders data, which is likely to be linked with an increasing number of refurbishments to office spaces taking place for employees returning to the office.

There was also a notable increase in the smaller sector of private industrial new work, which grew by 5.3% (£25 million). This continued to be strong over the last year and came from an increase in warehouses and distribution centres. This is further shown in the new orders data. Warehouses showed an increase likely to be linked to consumers change in shopping habits and online spending during the coronavirus pandemic.

Quarter-on-quarter change in construction output in Quarter 1 2022

Construction output increased by 3.8% (£1,636 million) in Quarter 1 2022, following the 1.0% increase in Quarter 4 2021. Outside of the coronavirus pandemic period, this is the strongest quarterly growth since Quarter 1 2017 (3.9%).

Both new work and repair and maintenance saw large increases in Quarter 1 2022; these increases were 2.8% (£768 million) and 5.5% (£868 million), respectively.

Seven of the nine sectors saw an increase in Quarter 1 2022. The largest contributors were non-housing repair and maintenance, and private housing in both new work and repair and maintenance. These sectors increased by 7.4% (£581 million), 5.2% (£484 million), and 4.5% (£277 million), respectively.

3.New orders in the construction industry in Quarter 1 2022

Total construction new orders decreased by 2.6% (£346 million) in Quarter 1 (Jan to Mar) 2022 compared with Quarter 4 (Oct to Dec) 2021. See our New orders in the construction industry dataset for more detail.

Despite the quarterly fall in new orders in Quarter 1 2022, new orders are still at a higher level than before the coronavirus (COVID-19) pandemic. Quarter 4 (Oct to Dec) 2019, which was the last full quarter not affected by the coronavirus pandemic. Compared with this, total construction new orders are now 13.7% (£1,563 million) higher, with all six sectors still above their pre-coronavirus pandemic level in Quarter 1 2022.

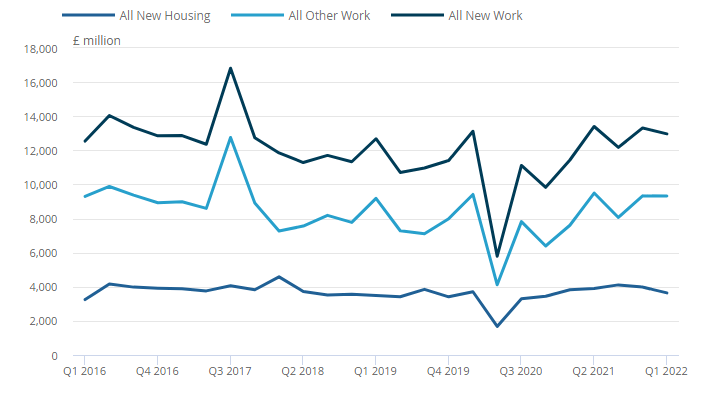

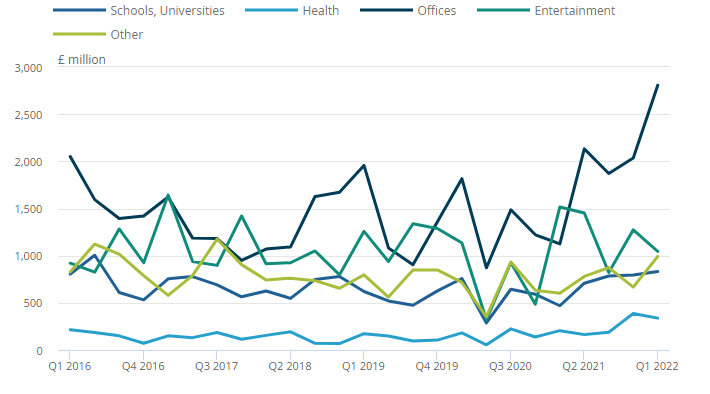

Figure 6: New orders saw a quarterly decline (2.6%) in Quarter 1 (Jan to Mar) 2022 but are still above their pre-coronavirus pandemic level

Components of new work, new orders, constant prices, seasonally adjusted, Great Britain, Quarter 1 (Jan to Mar) 2016 to Quarter 1 (Jan to Mar) 2022

The quarterly fall in Quarter 1 2022 mainly came from housing new orders, which fell by 8.5% (£339 million). Within this, private new housing decreased by 8.5% (£310 million).

All other work new orders (such as non-housing) also saw a smaller decline in Quarter 1 2022 of 0.1% (£6 million). The main negative contributor was private industrial new orders, which fell by 19.8% (£372 million). However, private industrial has been very strong in recent quarters, with the most recent year-on-year growth being 45.8% (£2,095 million) (Table 3). Over this period, the number and value of orders for warehouses and factories have increased significantly, particularly when compared with their pre-coronavirus pandemic level. For warehouses specifically, this is likely to be owing to more online retail.

Private commercial was one of two sectors (infrastructure being the other) to see quarterly growth in new orders in Quarter 1 2022. This growth mainly came from new orders for offices (Figure 7). Project level data suggests that a large number of businesses are carrying out office refits and refurbishments as workers return to the office.

Figure 7: Office new orders were the main contributor to growth in private commercial new orders in Quarter 1 2022

Components of private commercial, new orders, current prices, non-seasonally adjusted, Great Britain, Quarter 1 (Jan to Mar) 2016 to Quarter 1 (Jan to Mar) 2022

Table 3: Construction new orders main figures, Quarter 1 (Jan to Mar) 2022

Seasonally adjusted volume, £ million and percentage change, Great Britain

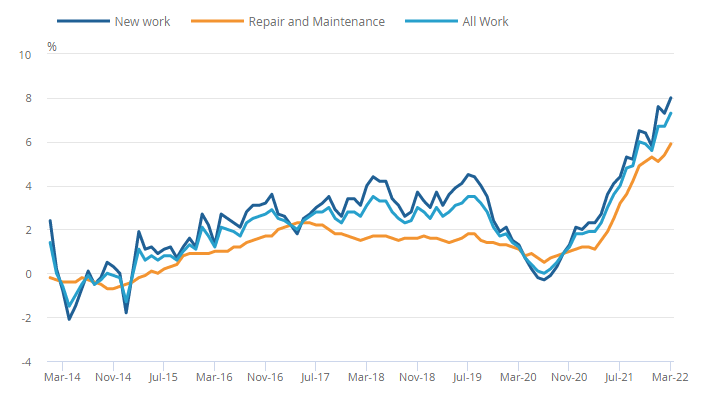

4.Construction output price indices in March 2022

Prices in the construction industry, as estimated by our Construction Output Price Index (OPI) dataset, increased by 7.3% in the 12-month period to March 2022. This was the strongest annual rate of construction output price growth since records began in January 2014.

This supports the anecdotal evidence received from survey returns to our Monthly Business Survey for construction and allied trades. These returns continue to suggest higher pricing of raw materials such as steel, concrete, timber and glass has contributed to the overall rise in material costs throughout Quarter 1 2022.

The monthly rate of prices for all construction work was 0.6% in March 2022, which increased from 0.1% in February 2022. However, it is still below the level seen in January 2022, which was a record monthly rise of 1.4% since records began in 2014.

Figure 8: Annual construction output price growth in March 2022 was at its highest rates of growth since records began in 2014

Annual rate of construction output price growth, percentage change, January 2014 to March 2022

New work

The Construction OPI for new construction work grew 8.0% in the year to March 2022.

The new work sector with the strongest annual growth rate of prices was new housing, which rose 10.9%.

Repair and maintenance

The Construction OPI for all repair and maintenance grew 5.9% in the year to March 2022. This is the strongest rate of growth for repair and maintenance output prices since records began in January 2014.

The repair and maintenance sector with the strongest annual growth rate of prices was non-housing repair and maintenance, which rose 6.6%.

That's a Wrap!

A lot of points have been covered and I hope this information in the report has been of some use to you. We do try to collate information from as many different areas as possible so please do refer to last months report as well for a crossover of information as some data sets are released at different intervals through out the year.

We will see you again soon!

If you are already a client of Saint, please feel free to discuss with your business development manager to discuss this report and to provide specific data for your sector.

The Construction Survival Guide

The only book you need to start up your construction business! The CSG becomes your new handbook offering everything that you need in order to create a successful construction business!

Claim Mine!

This article has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the provided content.

PS. Whenever you are ready, here's how to grow your construction business...

1. Join our Facebook Group which built completely for businesses within the construction industry. Real people, real support. - Now also available on LinkedIn.

2. Keep up to date with Construction Insider Providing you with industry insight, tips & tricks and much more to make sure you are ahead of your competitors!

3. When you are ready, Become a Saint Global client, and we will provide you with the highest quality solutions to effectively scale your construction business. Book your meeting here!

Written by the team at: