Construction Insider report covering the third quarter period up to October 2022

Modest growth across the construction industry

Construction enjoyed modest growth in output during August despite growing headwinds from energy and cost inflation in the economy.

Number crunchers at the Office of National Statistics also upwardly revised previous output figures for July. This moved the official figures from a 0.8% contraction in construction output to sluggish 0.1% growth for the month.

Revised output figures show construction output is holding firm

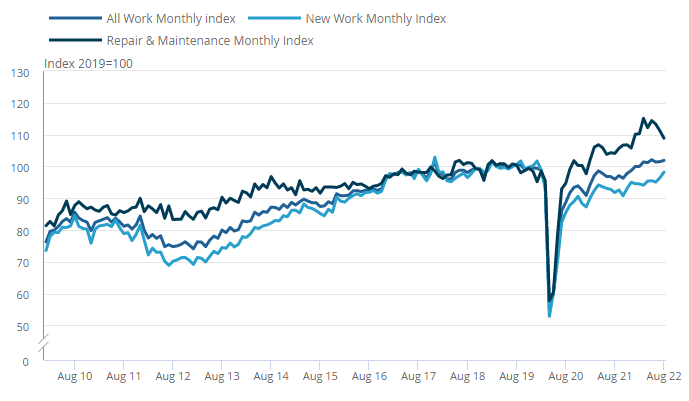

The August rise in monthly output came solely from an 1.9% increase in new work, with repair and maintenance falling 2.0% on the month. Main drivers were infrastructure, private industrial and private housing new work, which increased 5.3%, 4.3% and 1.7%, respectively.

The level of construction output is now 3.2% (£461m) above the February 2020 pre-coronavirus benchmark. Mark Robinson, group chief executive at procurement group Scape, said: “The construction industry continues to defy wider market conditions to contribute to what is now a near year-long run of growth in the sector. “As we come out of peak season however, it’s clear that we are set for a challenging winter as inflation continues to affect costs for private and public sector projects alike. “The Chancellor’s welcome energy support package will no doubt help, but project teams will need to work in close collaboration to manage costs as projects and pricing evolve. “Continued investment in public sector building projects will be vital for the well-being of the construction industry – and the country – as a whole this winter, with our figures showing that the sector delivered more than £1bn of social value last year alone.”

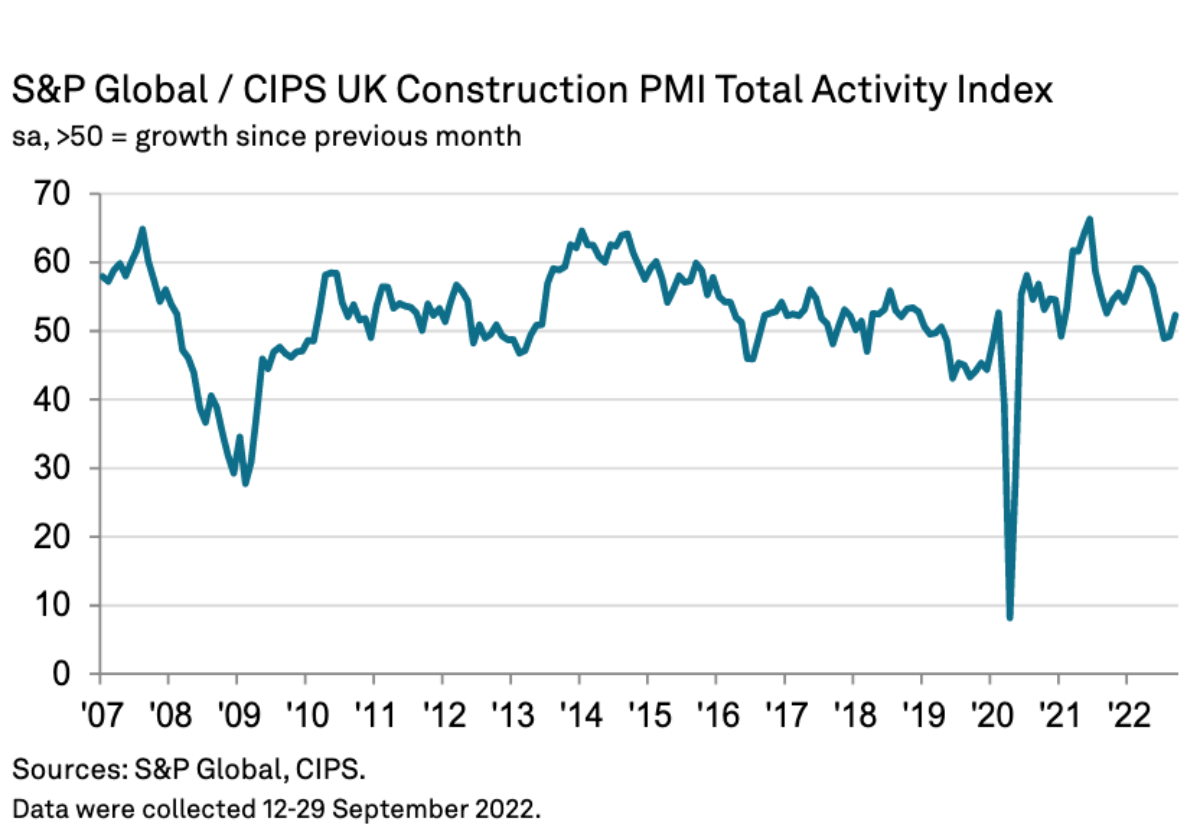

PMI Total Activity Index

UK construction companies saw a modest increase in business activity during September representing a return to growth after two months of falling output.

Optimism for future prospects dropped to its lowest level for two years as the prospects of higher interest rates and a downturn in the wider UK economy cast a cloud on construction.

The S&P Global/CIPS UK Construction Purchasing Managers’ Index hit 52.3 in September from 49.2 in August – above the crucial 50 no-change mark for the first time since June.

House building was the best-performing category in September (index at 52.9), with growth reaching a five-month high. Commercial work increased only marginally (51.0), while civil engineering activity (49.6) fell for the third month in a row.

Tim Moore, Economics Director at S&P Global Market Intelligence, which compiles the survey said: “UK construction companies experienced a modest increase in business activity during September, but the return to growth was fuelled by delayed projects and easing supply shortages rather than a flurry of new orders.

“Reports of delivery delays for construction products and materials were the least widespread since the pandemic began as greater business capacity and improved transport availability helped to ease pressure on supply chains.

“However, forward-looking survey indicators took another turn for the worse in September, with new business volumes stalling and output growth expectations for the year ahead now the lowest since July 2020.

“This reflected deepening concerns across the construction sector that rising interest rates, the energy crisis and UK recession risks are all set to dampen client demand in the coming months.”

Dr John Glen, Chief Economist at the Chartered Institute of Procurement & Supply, said: “Developments in the UK economy have given the sector food for thought as supply chain managers reported softer levels of buying last month and the new orders index slipped to its lowest since May 2020. “Though the headline index showed growth after two months in contraction, the devil lies in the detail pointing to lower customer confidence, a challenging UK economy and recession on the doorstep.“

Firstly, the rise in output has no sign of sustainable growth behind it as without new pipelines of work any gains will soon leak away. This was not lost on builders themselves who reported the lowest level of optimism since July 2020 about business opportunities in the next year.

“Secondly, the costs of doing business and the cost of living are still high and rising. More expensive energy and salary pressures to secure skilled staff have contributed

to additional inflation, though 21% of building companies in the sector were still hiring to maintain capacity for current projects.

“The housing sector remained the strongest performer in September although with interest rates rising and mortgage costs affecting affordability rates especially for first-time buyers, this will be an obstacle for house building to keep up the momentum as we approach 2023.”

ONS Report

1.Main points

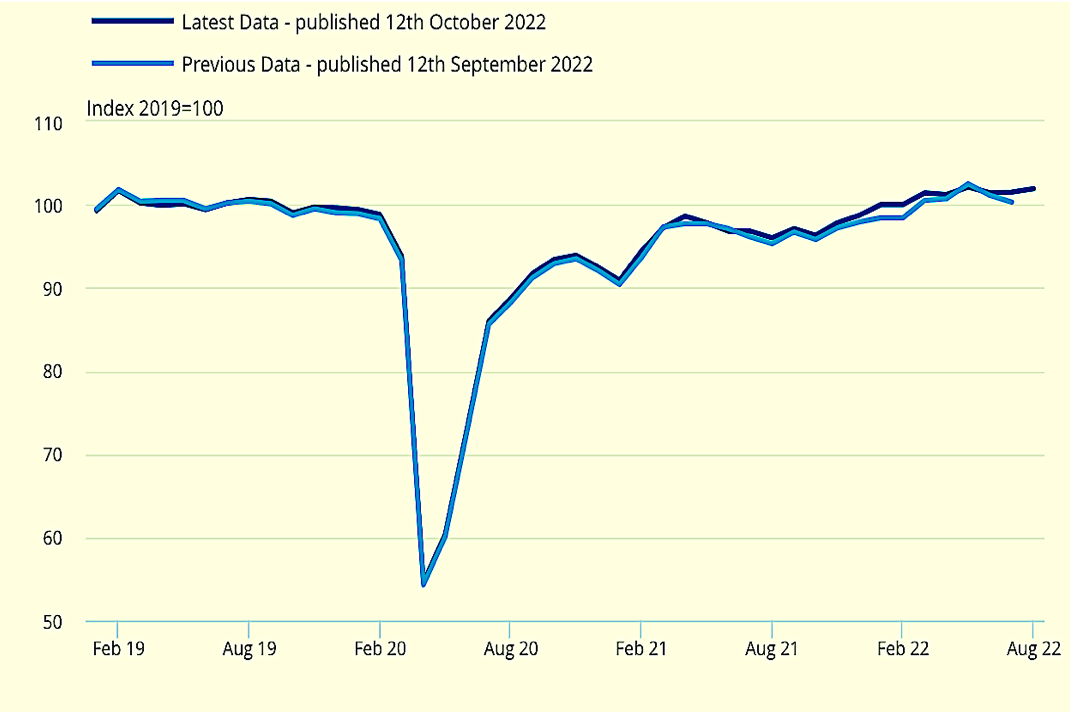

- Monthly construction output increased by 0.4% in volume terms in August 2022, which is the second consecutive monthly growth following the upwardly revised increase to 0.1% in July 2022; August 2022 is the second highest monthly value in level terms (£15,011 million), with May 2022 remaining at the highest level since records began in January 2010 (£15,035 million).

- The increase in monthly construction output in August 2022 came solely from an increase in new work (1.9%), as repair and maintenance saw a decrease (2.0%) on the month.

- At the sector level, the main contributors to the increase seen in August 2022 were infrastructure, private industrial and private housing new work, which increased 5.3%, 4.3% and 1.7%, respectively.

- The level of construction output in August 2022 was 3.2% (£461 million) above the February 2020 pre-coronavirus (COVID-19) level; new work was 0.7% (£69 million) below its February 2020 level, while repair and maintenance work was 10.6% (£530 million) above the February 2020 level.

- Alongside the monthly increase, construction output saw a slight increase of 0.1% in the three months to August 2022; this came solely from an increase seen in new work (1.6%) as repair and maintenance saw a decrease (2.4%), this is the tenth consecutive period of growth in the three month on three month series, however it is the slowest rate of growth since the three months to October 2021 that saw a fall of 0.7%.

- In this month's release, the earliest period open to revision is January 2011, and this is the first time the monthly path has been published that is consistent with the Quarter 2 (Apr to June) 2022 quarterly national accounts published on 30 September 2022.

2.Construction output in August 2022

Monthly construction output increased 0.4% in August 2022. This follows an upwardly revised 0.1% increase in July 2022. This is now the second consecutive increase in monthly construction output since June 2022 (0.6% fall), and is the second highest monthly value in level terms (£15,011 million) since records began in January 2010.

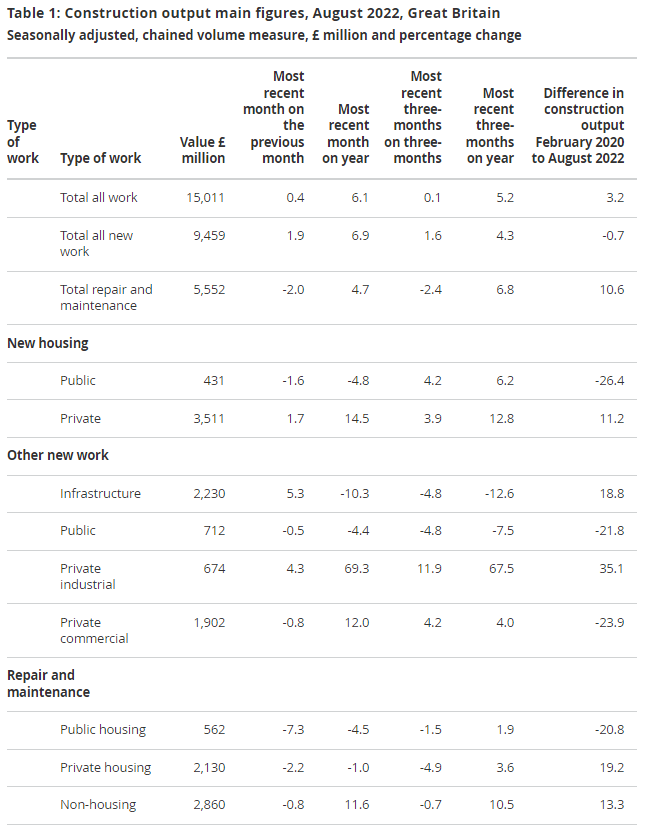

Figure 1: The monthly all work construction output index in August 2022 saw an increase on the month (0.4%), solely coming from a rise in new work (1.9%)

Monthly all work index, chained volume measure, seasonally adjusted, Great Britain, January 2010 to August 2022

Anecdotal evidence received from returns for the Monthly Business Survey for Construction and Allied Trades (MBS) and the Business Insights and Conditions Survey (BICS) continues the narrative around the increased prices for certain construction products. As in previous months, increased costs of products, most notably concrete, plaster, bricks, sand, gravel and asphalt-related products are mentioned. Alongside the continued narrative around prices, several businesses are continuing to mention labour shortages and the difficulty recruiting new staff is still continuing to have an impact.

The warm weather experienced in July 2022 (PDF, 128KB) has continued to be mentioned within the anectodal evidence received from returns for the MBS again this month, as the warm weather continued into August 2022 after the record breaking temperatures seen in July 2022. Businesses mentioned that for the construction industry the heat caused difficult working conditions. However, it was mentioned that more work was conducted in August 2022 than in July 2022 as the temperatures started to cool off in the latter part of the month, after the warm weather seen at the start of August 2022.

Month-on-month construction output growth in August 2022

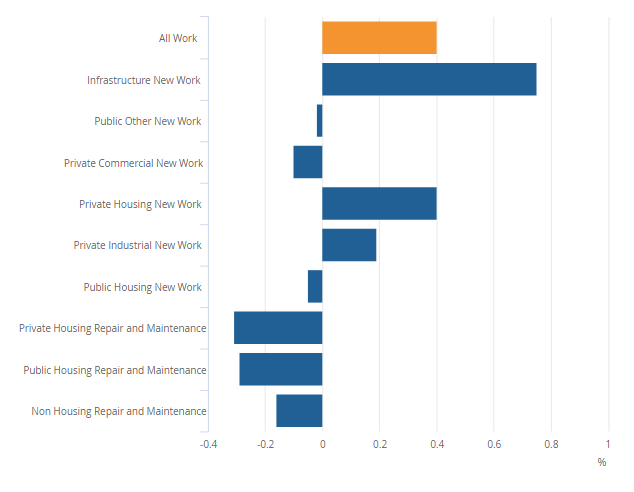

The 0.4% in construction output in August 2022 represents an increase of £60 million in monetary terms compared with July 2022, with three out of the nine sectors seeing an increase on the month.

Figure 2: All work saw an increase on the month in August 2022 (0.4%), with three out of the nine sectors seeing an increase

Contributions to monthly growth (August 2022 compared with July 2022), chained volume measure, seasonally adjusted, Great Britain, percentage points

Infrastructure, private industrial and private housing new work were the largest contributions to the monthly increase in August 2022, increasing 5.3% (£113 million), 4.3% (£28 million), and 1.7% (£60 million), respectively.

For the second consecutive month, all three sectors in repair and maintenance saw a fall on the month. The 2.0% decrease overall for total repair and maintenance is the fourth fall out of the last five months.

Anecdotal evidence gathered from businesses over the month suggested the narrative around the cost of living crisis was a major factor, as businesses and households are spending less on repair and maintenance work during this time. Many firms suggested that the high prices for construction materials meant some repair and maintenance projects were being put on hold (whether temporarily or permanently). In contrast, some new projects were continuing as costings were agreed prior to the recent price increases, and as such the construction firms were having to absorb these.

Three-month-on-three-month construction output growth in August 2022

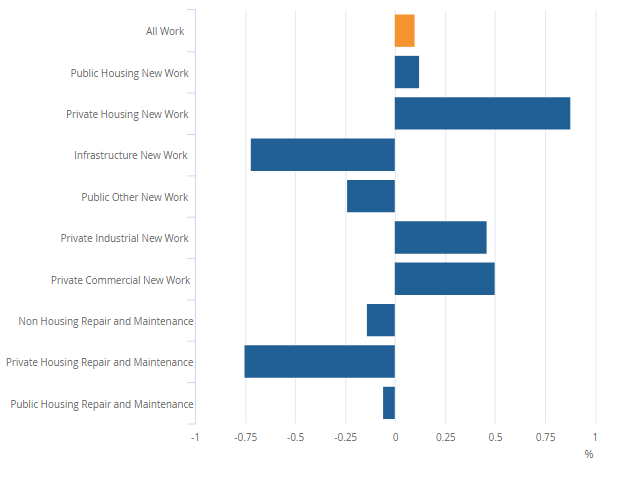

Alongside the monthly increase, construction output rose slightly by 0.1% (£25 million) in the three months to August 2022. This is the tenth consecutive increase in the three-month on three-month series but is this slowest rate of growth since October 2021 (decrease of 0.7%). The increase came solely from an increase in new work (1.6%) as repair and maintenance decreased (2.4%).

Figure 3: All work saw a slight increase in three months to August 2022 (0.1%), with private new housing the main contributor

Contributions to three-month-on-three-month growth (June to August 2022 compared with March to May 2022), chained volume measure, seasonally adjusted, Great Britain

Four out of the nine sectors saw an increase in the three months to August 2022, with the largest contributors being private industrial, private commercial and private housing new work. These sectors increased 11.9% (£208 million), 4.2% (£225 million) and 3.9% (£394 million), respectively.

Construction output grows In September

- Total industry activity rises for first time in three months

- Output growth linked to work on delayed projects

- Business optimism lowest since July 2020 as new orders stall

UK construction companies signalled a modest increase in business activity during September, which represented a return to growth after two months of falling output. However, subdued demand persisted, as signalled by the weakest trend for new orders since the recovery began in June 2020.

Looking ahead to the next 12 months, survey respondents remain cautious about their growth prospects. The degree of confidence towards the business outlook dropped to its lowest for over two years in September, mostly reflecting concerns about higher interest rates and a downturn in the wider UK economy. On a more positive note, supply shortages eased in September, with delivery delays the least widespread since February 2020.

At 52.3 in September, up from 49.2 in August, the headline seasonally adjusted S&P Global / CIPS UK Construction Purchasing Managers' Index® (PMI®) - which measures month-on-month changes in total industry activity - registered above the 50.0 no-change value for the first time since June. The latest reading was the highest for three months and signalled a modest overall increase in construction output. Survey respondents commented on a boost to activity from work on previously delayed projects.

House building was the best-performing category in September (index at 52.9), with growth reaching a five-month high. Commercial work increased only marginally (51.0), while civil engineering activity (49.6) fell for the third month in a row.

Survey respondents often commented on a strong pipeline of outstanding work, but incoming new orders remained relative scarce in September. Latest data signalled that new business volumes were broadly unchanged overall, which represented the worst month for new orders for almost two and-a-half years.

Construction firms cited slow decision making among clients and greater risk aversion due to inflation concerns, squeezed budgets and worries about the economic outlook.

Subdued client demand contributed to a marginal reduction in purchasing activity across the construction sector. Survey respondents also suggested that a turnaround in supplier performance had led to reduced inventory building. Latest data signalled the least marked lengthening of vendor lead times since the pandemic began.

Employment growth meanwhile accelerated from August's 17-month low. Around 21% of the survey panel reported a rise in staffing levels, while only 8% signalled a decline. Higher workforce numbers reflected efforts to boost business capacity, although construction firms continued to cite shortages of candidates to fill vacancies and strong wage pressures.

Average cost burdens increased sharply in September, but the overall rate of inflation eased to its lowest since February 2021. Survey respondents noted escalating energy costs and greater prices paid across the board for construction products and materials. Lower fuel prices and improved transportation availability were cited as factors helping to moderate the overall pace of cost inflation in September.

Finally, business optimism for the coming 12 months was relatively subdued in September. The latest survey pointed to the weakest growth projections since July 2020. While construction firms often commented on expected growth due to forthcoming new projects, many also suggested that recession risks and higher interest rates had weighed on confidence.

BMBI Report

Total Builders Merchants value sales were flat (+0.2%) in July 2022 compared July last year. Volume sales were -12.8% lower with price up +15.0%.

Total Builders Merchants value sales were flat (+0.2%) in July 2022 compared July last year. Volume sales were -12.8% lower with price up +15.0%.

There was no difference in trading days. Ten of the twelve categories sold more. Nine categories performed better than Merchants overall, including Renewables & Water Saving (+25.5%) Workwear & Safetywear (+20.2%), Kitchens & Bathrooms (+13.1%) and Plumbing, Heating & Electrical (+10.7%). Landscaping (-4.6%) and Timber & Joinery Products (-14.4%) sold less.

Total value sales in July 2022 were +13.3% up on the same month three years ago (a more normal year pre Covid). Volume sales fell -13.9% – prices rose +31.6%. With two less trading days this year, like-for-like sales (which take trading day differences into account) were up +24.1%.

Three of the twelve categories sold more than merchants overall. Timber & Joinery Products (+23.8%), Renewables & Water Saving (+18.6%) and Landscaping (+17.7%) did best. Other categories grew more slowly, including Heavy Building Materials (+12.3%), Kitchens & Bathrooms (+11.3%) and Plumbing, Heating & Electrical (+2.9%). Miscellaneous (-4.5%) was weakest.

Total Merchants sales were -2.6% lower in July 2022 than in June 2022. Volume sales were -5.2% down with price up +2.7%. With one more trading day like-for-like sales were -7.3% down this month. Renewables & Water Saving (+4.8%) grew most. Landscaping (-9.1%) was weakest.

July’s overall BMBI index was 151.5, particularly helped by Landscaping (195.5) and Timber & Joinery Products (171.0), with no difference in trading days. Almost all categories recorded indices exceeding 100, including Heavy Building Materials (147.0), Kitchens & Bathrooms (143.1) and Ironmongery (135.3). Only Renewables & Water Saving (90.4) fell below 100.

Total sales in May to July 2022 were +4.4% higher than in May to July 2021, with price inflation of +16.5%, volume down -10.4%, and no difference in trading days. Ten of the twelve categories sold more than merchants overall. Renewables & Water Saving (+20.0%), Kitchens & Bathrooms (+17.4%) and Workwear & Safetywear (+14.4%) did best. Timber & Joinery Products (-7.2%) was weakest.

Compared with the same months three years ago (May to July 2019), May to July 2022 sales were ahead +22.4%, driven by price (+30.0%) not volume (-5.8%). With two less trading days this period like-for-like sales were +26.4% ahead. All categories sold more. Two categories stood out: Timber & Joinery Products (+33.4%) and Landscaping (+31.3%). Heavy Building Materials (+20.5%), Kitchens & Bathrooms (+19.0%), and Plumbing, Heating & Electrical (+10.7%) grew less. Tools (+3.6%) was weakest.

Total sales in May to July 2022 were +4.2% up on the previous three months, February to April 2022, driven more by price inflation (+2.5%) than volume (+1.6%), with no difference in trading days. Ten of the twelve categories sold more. Landscaping (+8.8%) and Heavy Building Materials (+7.3%) did better than merchants overall. Decorating (+3.9%), Kitchens & Bathrooms (+2.2%) and Ironmongery (+1.2%) grew less. Plumbing, Heating & Electrical (-8.6%) was weakest.

The current year to date, January to July 2022, was +8.6% higher than January to July 2021. Volume sales were -6.7% lower with price up +16.3%. With one less trading day this year like-for-like sales were +9.3% higher. All categories sold more. Kitchens & Bathrooms (+20.8%) was strongest followed by Renewables & Water Saving (+20.7%). Plumbing, Heating & Electrical (+12.7%) Heavy Building Materials (+12.0%) and Decorating (+9.3%) grew more than merchants overall. Landscaping (+0.5%) was weakest.

Sales in the current year to date, January to July 2022 were +23.1% ahead of three years ago – January to July 2019. Price inflation was +26.7%, and volume was down -2.8%. With three less trading days in the most recent period like-for-like sales were +25.7% higher. All categories sold more. Landscaping (+39.4%), Timber & Joinery Products (+36.4%) and Renewables & Water Saving (+28.4%) performed better than Merchants overall. Tools (+4.9%) was weakest.

Total Merchants sales in August 2021 to July 2022 were +11.5% higher than in August 2020 to July 2021, with price inflation of (+16.5%), and volume (-4.2%). No difference in trading days. All categories sold more. Renewables & Water Saving (+17.2%) grew most. Kitchens & Bathrooms (+16.6%), Timber & Joinery Products (+14.8%), Heavy Building Materials and Plumbing, Heating & Electrical (both +11.9%) also did well. Workwear & Safetywear (+2.8%) was weakest.

Total Merchants sales in August 2021 to July 2022 were +20.4% higher than in the 12 months August 2018 to July 2019. With two less trading days in the most recent period like-for-like sales were +21.3% higher. Eleven of the twelve categories sold more with Timber & Joinery Products (+39.1%) and Landscaping (+36.1%) well out in front. Other categories saw lower growth including Heavy Building Materials (+14.7%), Kitchens & Bathrooms (+13.9%) and Plumbing, Heating & Electrical (+6.0%). Tools (-1.5%) was weakest.

That's A Wrap!

A lot of points have been covered and I hope this information in the report has been of some use to you. We do try to collate information from as many different areas as possible so please do refer to last quarters report as well for a crossover of information as some data sets are released at different intervals through out the year.

We will see you again soon!

If you are already a client of Saint, please feel free to discuss with your business development manager to discuss this report and to provide specific data for your sector.

The Construction Survival Guide

The only book you need to start up your construction business! The CSG becomes your new handbook offering everything that you need in order to create a successful construction business!

Claim Mine!

This article has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the provided content.

PS. Whenever you are ready, here's how to grow your construction business...

1. Join our Facebook Group which built completely for businesses within the construction industry. Real people, real support. - Now also available on LinkedIn.

2. Keep up to date with Construction Insider Providing you with industry insight, tips & tricks and much more to make sure you are ahead of your competitors!

3. When you are ready, Become a Saint Global client, and we will provide you with the highest quality solutions to effectively scale your construction business. Book your meeting here!

Written by the team at: