.jpg)

New Corporation Tax Rates - How To Calculate Corporation Tax in 2023

The current corporation tax rate for limited companies is 19% which is charged on your company’s profits no matter the level of those profits are.

From the 1st of April 2023, your corporation tax rate could be rising to 25% depending on the level of profits earned during the year. This Blog will cover the upcoming changes and give you time to plan ahead to mitigate the impact of the new rules.

New Corporation Tax Rates

For the Financial Year 2023 (starting 1st April 2023), the main rate of corporation tax will increase to 25% for limited companies whose profits exceed the “upper profits limit” of £250,000.

If your profits are below the “small profits rate” which is set at £50,000, your corporation tax rate will remain at 19%.

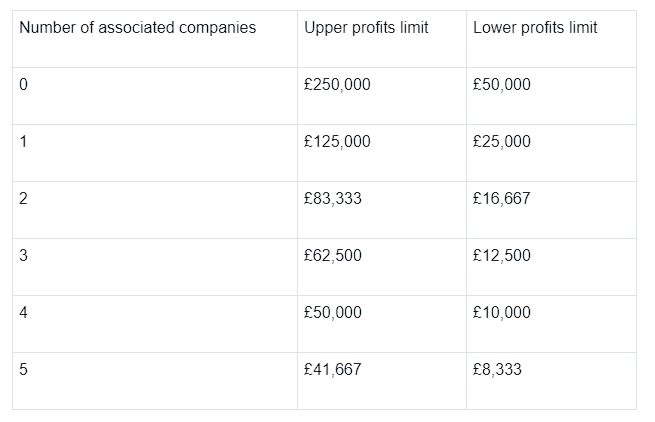

The lower and upper profit limits will be reduced proportionately where the accounting period is less than 12 months which is what is typically going to happen unless your new financial year for your company also starts on the 1st of April. The limits will also reduce where a company has one or more associate companies (we will cover this in further detail below).

This is where things get a little more complicated… companies whose profits fall between the lower and upper profit limits (reduced where appropriate as mentioned above) will pay corporation tax at the main rate but reduced by the marginal rate.

The marginal relief provides a gradual increase in corporation tax as your profit level increases through the lower and upper profit limits until the main rate of 25% is reached.

Calculating Marginal Relief

To calculate marginal relief there is a formula that needs to be used:

F x (U – A) x N

Where:

F is the standard marginal relief fraction (set at 3/200);

U is the upper limit;

A is the augmented profits; and

N is the amount of the taxable total profits.

Example 1: Marginal relief calculation

A Limited company prepares its account to the 31st of March each year. The company has taxable profits (and augmented profits) of £190,000 for the year to 31 March 2024.

The company has no associated companies.

As the company profit levels fall between the lower and upper profit levels, we need to consider the marginal relief.

Marginal relief will be calculated as follows:

3/200 x (£250,000 - £190,000) x 1

= 3/200 x (£60,000) = £900

The corporation tax payable by the limited company is £46,600 ((£190,000 x 25%) - £900).

This gives an effective rate of tax of 24.52%

Associated Companies

A company is associated with another company if at any time or any other time within the preceding 12 months:

- One company has control of the other

- Both companies are under the control of the same person or group of persons e.g. same shareholders such as spouses

Dormant companies are not included

Example

If you have one company with taxable profits of £40,000 and one company with taxable profits of £5,000, the company with taxable profits of £40,000 will not benefit from the 19% small profits rate as the profits are above the lower limit of £25,000 that applies to a company with one associate company - £50,000 / 2 = £25,000. This means that £25,000 is charged at 19% and the remaining at the marginal rate.

Planning Ahead: Mitigating The Impact

With the new rules coming into play from the 1st of April 2023, it is time to start looking at how you can mitigate the impact and put your business in the best position. Here are some of our top tips:

- Where profits exceed the lower profits limit (£50,000 profit), accelerate profits so they are taxable in Financial Year 2022 (so they are taxed at 19%) instead of the new Financial Year 2023 rates (up to 25%).

- If you are exceeding the lower profits limit, delay any expenses to Financial Year 2023 to secure a higher rate relief (i.e less tax being paid)

- If any losses have been made in previous years, consider whether it is more beneficial to carry them forward rather than carry them back. This will slow down the speed of the relief (but a lower rate) however carrying it forward will potentially give relief at a higher rate

- Consider the impact of having multiple companies (associated companies) and whether restructuring would be beneficial

If you need any support in implementing the above methods, please contact Saint Taxation - The Construction Industry Taxation Specialists.

The Construction Survival Guide

The only book you need to start up your construction business! The CSG becomes your new handbook offering everything that you need in order to create a successful construction business!

Claim Mine!

This article has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the provided content.

PS. Whenever you are ready, here's how to grow your construction business...

1. Join our Facebook Group which built completely for businesses within the construction industry. Real people, real support. - Now also available on LinkedIn.

2. Keep up to date with Construction Insider Providing you with industry insight, tips & tricks and much more to make sure you are ahead of your competitors!

3. When you are ready, Become a Saint Global client, and we will provide you with the highest quality solutions to effectively scale your construction business. Book your meeting here!

Written by the team at: